InDERmediate: The Grid Overview

The Intended Audience and What Will be Covered

This article and those that follow in the series are for anyone trying to level up their knowledge of the electricity grid and all of the technologies, rules, and regulation that surround it. It’s a complex industry with many players at the federal, regional, state, and local level. Stakeholders span investors, installers, entrepreneurs, policy makers, and the planet. For newcomers to the energy industry, it can take time to get up to speed on how it all works and how it is evolving. This series is designed to accelerate the energy learning curve. For each topic we cover, we will include both an article that explains the topic in detail with helpful visuals (and plenty of links for you to explore if you want to go deeper) and a podcast episode that condenses the article and has discussion compleimenting the article.

The first episode will provide a broad overview of the electricity grid and its key players; think of it like a “Grid 101” lesson. Future releases will cover specific topics in more detail, such as regulations and the role of DERs. The podcasts will have expert guests to provide insights and shed light on topics that are difficult to learn on the internet. The blog will have more detail, visuals, and links to subsequent information. We’re targeting “intermediate” (we say inDERmediate, get it?) energy enthusiasts, meaning the reader has done some individual research but wouldn’t consider themselves an expert. Are you a complete beginner? You’re welcome here! Our aim is to give you the foundation of knowledge you need in this article and accompanying episode so you’re up to speed with our future content.

The first episode is intended to cover the key topics related to the grid which means we cover a lot! Our goal is to be clear, not brief. We’ll start with the basics of electricity and the units you should know, then cover the three steps of the national grid, the operators, governors, regulators, and finally, how the grid is changing and the role of DERs. Like learning anything, you’re probably not going to understand everything immediately, that’s okay. You could reread the article, check out everything we link to in it, and look up similar resources online. If things still aren’t clear or you have feedback, please don’t hesitate to reach out to us, we would love to hear from you!

Note: Accompanying podcast episode

This blog post and the InDERmediate podcast episode “#2: A Farm to Toaster Grid Overview” accompany each other.

#2: A Farm to Toaster Grid Overview

Listen now (72 mins) | Summary Join Pam, Ben and James as they turn up the voltage on a fun, electrifying chat! Starting off with a quick dive into the difference between kW and kWh, the team then converts energy usage of different items in toaster SI units. They shed light on the journey of energy from generation to your home, in the very first squadcast game - dish out some …

The Basics of Electricity

Let’s start with the basics. Electricity is the flow of electrical power. But what is power and how does it flow? Power is the rate at which energy is transferred and it flows like water through a pipe. There are several factors that impact the flow rate of power. Today, we’ll focus on two: voltage and current. Stay with us here, we aren’t going to talk about too many equations. Physics gives us an equation to describe how power relates to voltage and current: power (P) is equal to current (I) times voltage (V), or in mathematical terms P = I * V. This one is important, we talk about power, voltage, and current a lot in the energy field.

Sticking with the pipe analogy, voltage is like the pressure of the water flowing through the pipe.

Credits: Lavin Hiranandani

Current is like the size of the pipe with water flowing through it.

Credits: Lavin Hiranandani

We know how power flows but how do we measure it? There are a few units you need to know, the unit of power, the Watt (W), and the unit of energy, the Watt-hour (Wh). Watt in the world is a Watt-hour? Don’t worry, that’s our only nerdy joke. Energy is simply the amount of power produced over time. Let’s get back to that water pipe analogy. Power is like the flow rate of the water through a pipe, or how fast the water flows, that is measured by the watt. Energy is like the amount of water that passes through the pipe, or the volume of water that accumulates into a bucket, that is measured by the watt-hour.

Credits: Lavin Hiranandani

There’s much more to this topic, like the role of frequency and resistance, but, for today, the focus is power and energy. It’s helpful to understand the units and typical scale of each. We use the International System of Units, SI for short (remember the days of high school Chemistry class?). This means we use standard prefixes like “kilo” or “mega” to represent scale. Most of the time in the energy field, we talk in terms of kilowatts (KW), which is 1,000 watts, and megawatts (MW), which is 1,000,000 watts or simply 1,000 kilowatts. To help you get an idea of the scale for various generators, check out this table.

The table above provides examples of power generation but how much power is consumed by certain devices and typical buildings? That’s right, another helpful table.

To wrap up, there are some practical things you should understand about electricity when it comes to our grid. First, supply (the amount of power being produced) must always equal demand (the amount being consumed). When supply and demand don’t equal, the frequency changes. Outside of a certain frequency, the grid begins to literally tear itself apart. For reference, the US and Canadian grid runs at 60 Hz and the European grid, like most of the world, runs at 50 Hz. Whenever you hear about large blackouts, like the ones in Texas in 2021, it isn’t that area losing power because it stops flowing but because it is being purposely turned off, or shed, by the grid operator to preserve that ever important frequency. Some people are temporarily losing power so permanent damage isn’t being done to the grid’s hardware.

If you’d like to go deeper on electricity, we suggest these resources:

Moving Electricity: The Three Steps of the Grid

Historically, there are three steps of the grid: Generation, Transmission, and Distribution. Traditionally, this has been a one-way street where power flows from the generation site through the transmission grid to the distribution grid. We’ve made a chart to help you visualize this:

Credits: Lavin Hiranandani

Generation

Generation refers to electricity generation that can be transmitted, distributed, and consumed. Historically, generation happens in bulk at what we call the “utility-scale”. This means individual, centralized power plants with BIG power output capacity, often more than 50 megawatts (the biggest power plant in the US is the Grand Coulee Dam at a whopping 7,000 MW). When we talk about generation in the energy field, the “mix”, or the composition of sources of where that power is coming from, is often discussed. This has become more prevalent in the global discussions surrounding climate change. So, what is the generation mix in the US? Glad you asked! The EIA, the US Energy Information Administration, reports about the energy field in depth (if you’re ever curious about the numbers surrounding something, we recommend checking out their great site). Here’s the generation mix of the US in 2021, compliments of the EIA:

Fossil fuels (61%): coal, natural gas, and petroleum

Nuclear energy (19%)

Renewable energy (20%): (wind, hydro, solar, biomass, geothermal)

The generation mix powering the grid varies throughout the country. For example, there is a lot of hydropower in the Northwest of the US, but very little in the Northeast of the US. This has to do with geography and weather. If you’re curious about where your power is coming from, check this out. Big (>50 MW) generation is most often connected to the transmission grid, which is composed of high power (>100kV) voltage lines.

Transmission

Transmission refers to the transportation of electricity across long distances from generators to population centers by high voltage power lines. These are the huge transmission towers you see on the side of the highway. The transmission system is like the national highway system of the grid! The on and off-ramps to this electricity highway are substations. Substations contain transformers that change the voltage of the power being transmitted. This is important; transformers are at each stage of power’s journey. They “step up” the power after it is being generated so it’s a high voltage for the transmission grid, they “step down” the power coming from transmission grid into the distribution grid, and they further step down the power right before it enters buildings. Substations can be seen along actual highways, they look like this and usually have a few transformers and tons of electrical wires. The transmission hardware starts and stops at these substations when they take electricity from generators, and deliver it to the distribution networks.

The transmission system is managed at the regional level by entities called Balancing Authorities (BAs) whose main job is to keep the system “happy” at that special frequency of 60 Hz. To achieve this goal, balancing authorities forecast demand and dispatch generators to meet that demand (because that supply must always equal demand). The balancing authorities are the air traffic control of the grid. NYISO is one example of a balancing authority (we’ll talk about them later). Check out that control room!

The New York Independent System Operator’s control room taken from their LinkedIn page.

In regulated areas, the utility is a monopoly and thus is responsible for the generation, transmission, and distribution of power to customers, and plays the role of the balancing authority. In deregulated areas, there is market competition and the utility has ceded balancing authority to the ISO or RTO. ISO? Deregulated? Don’t worry, we’ll talk about those too.

Distribution

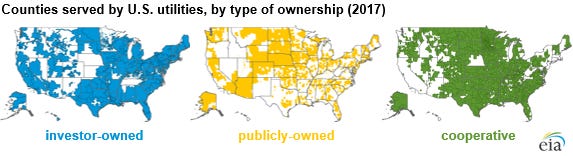

Many different monopoly utilities control the wires between the electrical substation and the homes and companies of Americans. Think of distribution like a neighborhood subdivision where the speed limit is only 20 miles per hour. In the US, the operators of the distribution network are either investor-owned utilities (IOUs), municipal-owned utilities (MOUs), or co-ops. Internationally, Distributed System Operators (DSOs) play a similar role. If you haven’t noticed, the energy field loves acronyms.

Investor-owned utilitiescompanies that charge “ratepayers” (that’s their name for you, their customer) are incentivized by building out as much infrastructure as possible. Municipal-owned utilities are owned and operated by the state or local government and are often smaller, non-profit entities. Co-ops are typically owned by their members. The structure depends on where in a state or country you live. For example, investor-owned utilities tend to serve large population centers and their surrounding communities, while co-ops tend to occur in more rural parts of the country. See a map of all the electricity providers in the USA here.

There’s a lot of change coming to the grid at the distribution level. We can’t wait to tell you about it.

The US Grid

When understanding the US grid, it is helpful to consider the geography of the system at different levels.

Interconnections

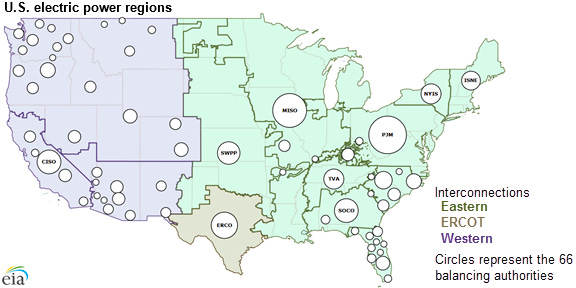

The electric grid of the United States is actually three separate grids, or “interconnections,” with minimal transfer of power between them: the Eastern Interconnection, the Western Interconnection, and the Electric Reliability Council of Texas (ERCOT). The borders of the interconnections are often referred to as the “seams” of the grid. These interconnections result in physical limitations to the system. For example, It is very challenging, if not impossible, to produce electricity in California and consume it in New York. Think of the three interconnections as three completely separate systems.

Balancing Authorities

Balancing authorities (BAs) are regional entities within interconnections that do the day-to-day operations of the system. They dispatch generators, predict demand, and keep the grid happy at 60 Hz. If you want to learn more about BAs (all 66 of them in the US), check out these great links by the EIA: here and here. Balancing authorities are typically ISOs/RTOs, or utilities.

ISOs/RTOs

Independent system operators (ISOs) or regional transmission organizations (RTOs) function as special balancing authorities with extra responsibilities. ISOs/RTOs are, for all intents and purposes, the same thing and you will often hear the terms used interchangeably. ISOs/RTOs are non-profit, independent organizations who manage the transmission system. They dispatch generators using a competitive market, run models and forecasts to make sure that there is always going to be enough power (and not too much) on the system to meet demand, and have certain transmission planning requirements from the federal government. In summary, ISOs/RTOs are responsible for:

Managing physical infrastructure

Keeping the power grid balanced between generation and consumption

Dispatching power plants and planning for expansion and new resources

Ensuring sufficient generation and backup power is in place to meet demand

Managing and relieving congestion within transmission lines (congestion refers to a lack of transmission line capacity to deliver electricity without exceeding thermal, voltage, and stability limits designed to ensure reliability)

Controlling transmission facilities for voltage, monitoring, and switching in and out of service

Managing restructured (competitive) power markets

Providing the software platform for the electricity market transactions

Managing the process for buying and selling electricity

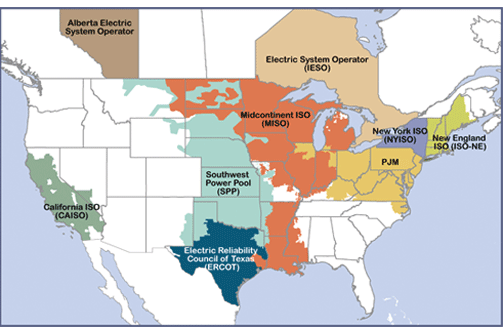

ISOs/RTOs came to operate competitive wholesale power markets through a process called restructuring. In the 1990s, the electric power industry began deregulating, or restructured, by shifting from a monopoly utility model to one based on competition. This was intended to increase efficiency and lower prices. At the wholesale level, this goal was realized by incentivizing utilities to cede the control and operation of their transmission assets to ISOs/RTOs. Functioning as intermediaries which separate the production and delivery of electricity, these new entities dispatched generators to serve load based on cost and allowed merchant generators owned by independent power producers to fairly participate in the market. The regions that have been restructured are represented by the seven ISOs/RTOs shown in color in the map below, with FERC as a resource to learn more.

Utilities

Utilities, often referred to as Load Serving Entities (LSEs), are the actors within the grid that people tend to be most familiar with. For better or worse, every month you probably get a bill from yours in the mail! Utilities operate the distribution system (the “poles and wires” of the grid) and sell power to customers. They also often run programs such as energy efficiency (trying to get end customers, ratepayers, to consume less energy) and demand response (stay tuned, this might become an article and episode as part of our series). Depending on the state, they may own and operate transmission lines, and, in most cases, generate power.

{kind=link}

{kind=link}

A map of electric utilities in Michigan.

There’s so much more for us to talk about here, we’re restraining our inner nerds! There are lots of other ways to visualize the grid, like sub-LAPs, zones, and nodes, but those are outside the scope of this article.

Buying and Selling Electricity: Energy Markets

There are two kinds of electricity markets in the US: regulated and deregulated.

Regulated Markets

In regulated markets, a monopoly utility controls generation, transmission, distribution and serves as the only retailer to customers. As a result, there is no energy choice and all buying and selling of electricity occurs on a customer’s electricity bill. The two main components of an electricity bill are:

Electricity supply: the cost of the generated electricity used by the customer

Electricity delivery: the cost of everything it takes to transport electricity from the point of generation to the customer using the transmission and distribution system

Utilities use meters located on every building and home to measure customer electricity usage and translate that usage into bill charges according to their tariffs. Bill charges as outlined by tariffs are normally a function of electricity usage (usually measured in kWh) and demand (usually measured in kW). In regulated markets, the rates charged to customers are usually regulated at the state level by the state’s public utility commission (PUC).

Deregulated Markets

There are two levels of market deregulation, wholesale markets and retail markets.

Deregulated Wholesale Markets

In areas with deregulated wholesale markets, both monopoly utility and non-monopoly generators (these are companies that are owned independently and not by a utility) sell electricity into a wholesale market operated by an ISO or RTO. Deregulated wholesale markets can be thought of as the buying and selling of electricity from a generator to an electricity retailer (someone who buys electricity from a wholesale market and resells it to you, the customer). Retailers can be monopoly utilities or non-monopoly companies, normally called retail electricity providers (REPs). These energy transactions occur at the transmission portion of the grid, and the market is operated by an ISO or RTO.

Map of North American deregulated wholesale markets. Market territories are the combination of all utility territories within them. If an entire state is not in a wholesale market, it's likely because one of their electric utilities voluntarily joined and is a multi-state entity. Learn more here.

ISOs and RTOs normally run three kinds of markets:

Energy markets: generators offer electricity into the market where it is purchased by retailers at the market rate. This is what you typically think of for an energy market. 95% of all energy is sold one day ahead with the remaining 5% sold in real-time, usually once every hour and every five minutes.

Capacity markets: markets that incentivize the construction of new generators and ensure that there will be enough supply to meet demand. These markets compensate generators for their promise to be available to produce electricity in the future, or for the capacity they contribute to the system. Retailers are required by North American Electric Reliability Corporation (NERC) to purchase a safety factor of additional electricity during extreme grid events like hot summer days and extreme winter storms. This electricity has traditionally been provided by peaker plants.

Ancillary services markets: markets for services not already handled in the energy and capacity markets like helping to maintain grid frequency and providing short term backup power if a generator fails.

Still not making sense? That’s okay. Let’s explain with a fun analogy: RTOs are essentially bars (who said energy can’t be fun?). Capacity markets are the cover fee that you pay to get in the door and ensure that the bartender will sell you drinks, energy markets are the actual drinks you buy, and ancillary services are the bar peanuts and popcorn that you eat on the side to keep you from getting alcohol poisoning. This analogy isn’t perfect but it can still be helpful.

Deregulated Retail Markets

In deregulated retail markets, determined at the state level, monopoly utility and non-monopoly retailers buy and resell electricity supply to customers like you. Deregulated retail markets can be thought of as the buying and selling of electricity from a retailer to a consumer. These energy transactions occur at the distribution portion of the grid.

For a breakdown of customer retail choice in all 50 states, click here.

In deregulated retail markets customers can choose to buy their electricity supply from a non-monopoly retailer, often called a retail electricity provider.

Wholesale markets? Retail markets? What’s the difference? We made a handy graphic to help differentiate them.

Credits: Lavin Hiranandani

If you’d like to go deeper on electricity, we suggest these resources:

Grid Governance

Governance of the electric grid is a mess, but that’s what makes it fascinating! Only in the world of electricity policy will you see a U.S. Representative (Sean Casten, D-IL) stand in front of Congress with a “Hot FERC Summer” album cover while he declares his love for the agency.

“Well I rise today to declare the start of hot FERC summer…It’s time for them to be the MVP.” (Source).

Before we get to the FERC madness, let’s begin with the big picture. One of the most prominent themes throughout the electricity sector is the question of whether or not something is regulated by the state or federal government. In the 1900s, when many of our basic energy laws were passed, this distinction was very cut and dry. Increasingly, this “bright line” between the two spheres of jurisdiction is becoming blurry. This is especially relevant to distributed energy resources (we’re almost to that section, don’t worry!) for reasons that will be covered in depth in future articles and episodes.

Energy regulation in the United States has historically had three goals:

Economic success

Safe, cheap, and reliable electricity

Energy independence

Increasingly, there has been consideration of a fourth goal, but no clear consensus.

Environmental goals

In general, the transmission system is regulated by the federal government (there are certain cases where it’s not). The distribution system is regulated by the state government (except for when it’s not). Wholesale transactions of power occur on the transmission system. Retail transactions of power, or transactions between the utilities and the consumer, occur on the distribution system. When talking about regulation and governance, it’s important to remember that things are rarely clear and are often very messy.

The Federal Energy Regulatory Commission (FERC)

The arm of the federal government that regulates the transmission system is the Federal Energy Regulatory Commission (FERC). FERC is an independent agency who is tasked by the Federal Power Act of 1935 (FPA) to ensure “just and reasonable” rates in wholesale transactions of power. Today, any sale of power on the transmission system is considered a wholesale sale because the world got complicated, electrons follow the laws of physics, and judges are legal scholars and not physics professors.

In a regulated wholesale market (i.e. the utility is still a monopoly as far as the transmission system is concerned), wholesale transactions must be filed and approved by FERC (section 205 of FPA). If FERC determines that the price is unjust and unreasonable and unduly discriminatory, then they will be happy to “step in and fix” that for you (section 206 of FPA). We don’t intend to make the government sound like some mafioso but just know that, yes, they do call the shots.

In a deregulated wholesale market (i.e. the ISO/RTO is running the show), any transaction within that system is generally considered to be just and reasonable and not unduly discriminatory. FERC does not regulate individual transactions. They regulate the market design itself.

FERC has one other important job. They oversee the electric reliability organization that has regulatory authority over the reliability of the bulk power system. This entity is the North American Electric Reliability Corporation (NERC). If FERC can’t explicitly tell you to do something when it comes to reliability, there is a decent chance that NERC probably can. Unless you do bulk power systems planning and deal with balancing authorities/RTOs/ISOs, you probably won’t deal with NERC too much. If you’re interested in regulation (for some weird reason), then stay tuned because we’ll be covering it in future installments!

Public Utility Commissions (PUC)/Public Service Commissions (PSC)

The distribution system and any retail sales of power are regulated by the state government. This is generally done by the state’s public utility commission (PUC), which is sometimes also called the public service commission (PSC). Back in the day, the state government made deals with utilities called regulatory compacts in which they gave them exclusive franchise rights to sell electricity to an area. This came with the tradeoff that the PUC would have the authority to set the price of electricity that the utility can charge to customers. Similarly, the PUC also sets the return on investment that the utility can get from the ratebase (their customers) when it builds new infrastructure. This process is called ratemaking.

The Big Changes Coming to the Grid

We are at a very unique and special point in history. There are some big changes coming to the electricity grid and they can be broadly characterized into three main groups: renewables, distributed energy, and information technology (computing). They are each going to have different effects but all present unique opportunities.

Renewables: from on-demand fossil fuels to variable generation with solar and wind

Distributed energy: from a one-way centralized model to a bi-directional decentralized model

Computing: from analog to digital with a bunch of software and AI

These changes are not theoretical, they are already happening! Climate change and the need for resilient and affordable energy make change more urgent. One outcome is increased electrification (think cars, homes, factories), which will significantly increase the amount of electricity that is consumed. The grid needs to be ready for it. Let’s dig in!

Renewables

The first big change coming to the grid is more power generation coming from renewable resources. This is important because it means clean, not “dirty”, energy can be delivered to your home. The renewable sources today are: solar, wind, hydro, biomass, geothermal. Wind and solar (both photovoltaics and concentrated solar power) are the driving forces behind the explosion in renewables, accounting for more than 70% of new generation. Renewables are dominating because their economics make them lower cost than even the lowest cost coal (here’s just one link but we encourage you to nerd out). Calculating the value of renewables gets a little tricky. Almost all of their cost is CapEx (up front) versus fossil-fuel generators that have CapEx (up front cost) and significant OpEx (ongoing cost). OpEx and CapEx? Read this. Renewables do not require fuel, just limited maintenance over time. Fossil fuel-burning generators cost a lot upfront (generally less per KW compared to renewables) but most of their cost comes over time through fuel to power their generators. To compare renewables with traditional power sources, we use something called the Levelized Cost of Energy (LCOE). Don't worry too much about LCOE right now. Wind and solar are great, right? They are, but they come with certain challenges. They are:

Non-dispatchable: wind and solar are not “dispatchable”, meaning that we can’t control them and make them produce power whenever we want like with traditional generators. We can’t control the wind or the sun.

Intermittent: renewables are “intermittent” meaning they can’t constantly produce power 24/7; the wind isn’t always blowing and the sun isn’t always shining.

Location-dependent: can’t install wind and solar wherever we want; the weather patterns aren’t favorable enough to generate an economical return at every location we wish.

What about hydropower? Hydro is great but it can only be installed in a few locations, rivers, though it is dispatchable and largely not intermittent. Though it is not renewable, it is still important to mention nuclear power as it is a clean source of energy. Nuclear helps make up for some of the shortfalls of intermittency. Nuclear accounted for 19% of electricity generation in 2021. What about batteries? Yes, batteries (aka “storage”) will be very important in the future, but we are not focusing on storage here as that power has to originally come from somewhere..

This all sounds great, let’s race into the future! Well, not so fast. Transitioning to non-carbon-emitting sources means overcoming intermittency and the inability to dispatch the renewables. Beyond that, when there is a change to an industry worth over a trillion dollars a year that is so important to the broader economy, there is going to be pushback. Pushback comes from many sources; from scientists and engineers genuinely concerned about reliability to entrenched interests concerned with maintaining the profits for their fossil fuel generators and their supply chain. The pushback gets political so we’re going to stay out of it. If you want to learn more, we encourage you to do your own research. Be careful; there are a lot of low quality resources out there.

Distributed Energy

The second big change coming to the grid is distributed energy. We’re talking about distributed energy resources (DERs), the entire point of this group, the DER Task Force! DERs are exploding in terms of installations. We use the term “penetration” to refer to how much energy is being generated by a certain source relative to the entire grid. So what is a DER? We’ve discussed FERC so we’ll use their definition:

DERs: small-scale power generation or storage technologies (typically from 1 kW to 10,000 kW) that can provide an alternative to or an enhancement of the traditional electric power system. They may include electric storage, intermittent generation, distributed generation, demand response, energy efficiency, thermal storage or electric vehicles and their charging equipment.

The most common DERs are rooftop solar, electric vehicles, and battery systems for buildings; here’s a quick list of more DERs. As we’ve discussed, the distribution grid moves power to end consumers. At the end of the power’s journey is the grid meter. Your home and all buildings on the grid will have one. It is used to measure how much energy is consumed by the building. The meter creates a divide that we refer to as the “front of the meter” vs “behind the meter”.

Front-of-the-meter: typically refers to assets that are directly connected to the distribution grid

Behind-the-meter: refers to the other side of the meter, the building(s) and equipment that is usually owned by the end consumer (individuals or businesses).

We’ve talked about power flows being one way because that’s how the grid has operated for over a century. With DERs, power can now flow in two directions. This is a big deal. The grid was not designed to operate with two-way power flows. David Roberts has a great article discussing grid scenarios that could help manage the complexity that comes with many new participants in the energy ecosystem. Power generation becoming distributed has many interesting implications. One is that it drastically lowers the barrier to entry for people and companies to generate power for the grid–and be compensated for it. This opportunity for people to create new income streams has become an area of concern for policymakers.

Credits: Lavin Hiranandani

Did you really think a group called the DER Task Force is going to spend one short paragraph talking about DERs? Think again. The penetration of DERs is exploding. There are many reasons for this but the main one is their rapidly improving economics. Different DER technologies are at different stages in their lifecycle but all are growing fast. It is important to understand that everything about DERs is diverse, from the technology to the usage, characteristics, economics, sizes, and install locations. Rooftop PV is by far the most mainstream DER. Battery storage is next. You can think of battery storage as stationary batteries in a home, like Tesla Powerwalls. Batteries can move too and that’s a big deal. Electric vehicles, EVs, may become the most popular DER in the US. There are currently hundreds of millions of cars in the country. Trying to forecast how fast EVs may penetrate the grid gets complicated so we’re going to stay in our lane. No pun intended (we’re better than that).

We’ve talked about conventional DERs, or physical devices purpose-built to produce power. DERs can also be household appliances with a little bit of software. The most commonly used appliances that double as DERs are water heaters and heat pumps. As strange as it sounds, DERs can also be virtual. HVAC (heating, ventilation, and air conditioning) systems, present in almost every building, can become a DER with software and machine learning (AI). HVAC systems are controlled by smart thermostats that can be adjusted up or down to modulate the energy consumed by the system. Similar to how batteries can be charged and discharged, HVAC systems can be controlled to “charge” or “discharge” (treating the air in the building like a battery). This is an important knob, especially in the peak of summer or winter when heating and cooling systems operate at their max. DERs create value on their own but they can create a lot of value when we make them work together. One current form of making them work together is a Virtual Power Plant (VPPs). VPPs are still in their early days and the regulations and economics need to be worked out. With these unconventional and virtual DERs, there is a human aspect to be considered as well; after all, humans are using them. DERs are surprisingly cool, right? We think so.

Computing

There have been few things in human history that have had such an impact and at such a rapid pace as the revolution in computing (information technology) has. Computers have gotten cheaper, more powerful, more efficient, and smaller faster than ever seen in the history of human technology. With these advances, computing is in places previously unimagined. That includes energy. Computing hardware is the foundation for layers of technology. Computers are the foundation for software; software creates a tremendous amount of new value and enables sophisticated logic and processes to improve the grid and the user experience. Software is the foundation for data; data generated from the software and sensors connected to the grid enables many new use cases and improvements. Data is the foundation for AI; AI is still young but is already creating new use cases. If you thought computers developed rapidly, AI is moving even faster.

The first broad wave of computing/IT in energy happened in the 2000s with the deployment of smart meters, also called advanced metering infrastructure (AMI). Smart meters are electricity meters that connect to a network (usually cellular or radio mesh) and broadcast their readings in short intervals (often every 3 seconds) to utilities. AMI helps utilities reduce costs by not sending people to read meters, but it enables more than this. It allows utilities to use more advanced rates and vary how much they charge for energy every hour to incentivize load shifting. Don’t be mistaken, computers and software have run the grid for decades, especially in transmission. We talk about AMI because it is the first large-scale penetration. AMI enables interesting things but is relatively simple and largely just broadcasts meter readings. Smart meters are getting more powerful with onboard processors; this enables use cases at the grid edge. Other grid edge computing devices are home energy monitors. Appliances and other large consumers of energy are getting their own processors and internet connections (sometimes called “smart” devices but this term is often unclear). Fridges, water heaters, heat pumps, and HVAC systems, to name a few, are now connected and able to be controlled by external software. DERs usually have their own processor and internet connection for external control. If a device can be controlled, it can be optimized. This is a big deal. As these devices penetrate the grid, the grid will no longer be just a bunch of hardware, but a connected system of controllable and optimizable devices.

Conclusion

We covered a lot of ground in this article. It’s dense and has a lot of links so feel free to bookmark it and visit back often. It’s okay if you don’t fully comprehend everything after your first read, that’s natural with learning about any topic. If you have any questions or feedback, please reach out to us. We would love to hear from you! You can reach us on the DER Task Force official Slack (channel ID: C045GH89E7R; it’s called “#indermediatepodcastgang” but that name could always change). We hope we have sparked some interest in you! If we have, definitely check out our other articles and episodes in this series. We’re still deciding on some of the topics and guests, so, if you have any ideas, we would love to hear them! Please don’t forget to subscribe to the DER Task Force Substack account (it’s free but you can choose to donate) and share this with anyone who you think will like it. Thanks!

This article was written by Chantelle Domingue, James Gordey, Ben Hilborn, Charles Jurczynski, Wyatt Makedonski, and Pamela Wildstein.

Acronyms

DERs: Distributed Energy Resources

ISO: Independent System Operator

RTO: Regional Transmission Operator

BA: Balancing Authority

TSO: Transmission system operator

IOU: Investor owned utility

Munis: Municipal utility

DSOs: Distribution system operator

FERC: Federal Energy Regulatory Commission

NERC: North American Electric Reliability Corporation

PUC/PSC: Public utility commission/public service commission

Hi all, thank so much for this, I'm a newcomer combing through for the 2nd time!

One suggestion re: "Bill charges as outlined by tariffs are normally a function of electricity usage (usually measured in kWh) and demand (usually measured in kW)." Newbz might not understand what demand means here separate from usage. Easily googleable but could be worth a quick call-out! I'm also curious how much relatively high bills get driven by high usage versus high demand.